News analysis: As bitcoin bounces, blockchain breaks through

David Reed

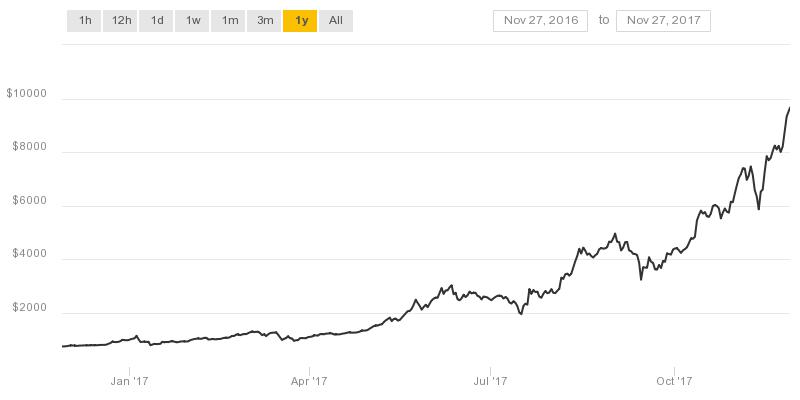

David ReedThis year has seen bitcoin in vertical take-off, only to undergo a number of reversals before resuming the skyward trajectory of its value. Between digital hipsters and professional currency traders, the prevailing view is that its time has come - provided a few technical hitches can be resolved. Its current valuation just shy of $10,000 seems ample proof of that.

If you are not a code miner hoping to cash in, you might find a more business-focused alternative with better stability in the technology principles that underpin bitcoin. Blockchain (or distributed ledger technology - DLT) is also reaching that crucial tipping point when enthusiastic advocacy converts into real-world adoption. Today’s Blockchain Summit at Olympia is expecting 1,500 delegates, a sign of impending maturity for this solution. So, too, is the presence of speakers from the likes of Barclays, Bosch and BUPA among the bright-eyed developers and vendors showcasing their DLTs.

If you are not a code miner hoping to cash in, you might find a more business-focused alternative with better stability in the technology principles that underpin bitcoin. Blockchain (or distributed ledger technology - DLT) is also reaching that crucial tipping point when enthusiastic advocacy converts into real-world adoption. Today’s Blockchain Summit at Olympia is expecting 1,500 delegates, a sign of impending maturity for this solution. So, too, is the presence of speakers from the likes of Barclays, Bosch and BUPA among the bright-eyed developers and vendors showcasing their DLTs.

So has blockchain become credible and proven itself to be a deployable technology you can pitch to your board with confidence? Or does the continued association with a yo-yoing currency as loved by gangsters as it is by cryptocurrency fans still present an obstacle?

Blockchain is making a land grab

Dubai has announced its intention for all government transactions to be carried out across its blockchain-enabled Smart Dubai system by 2020. If that seems like a reach, consider that all local real estate contracts have been migrated into blockchain already, with power and water contracts due to follow shortly.

This is helping to draw inward investment because of the transparency and confidence it delivers. “Land registry transactions are perfect for the blockchain and, as the Dubai Land Department says, ‘this technology will allow investors residing in and around the world to verify property data that is backed by timestamp signatures enhancing the accuracy of data, the credibility of investment transactions and the transparency and clarity of the market’,” noted Baroness Michelle Mone, who launched the first bitcoin-priced international luxury property development in Dubai last month.

TrustMe has launched as a peer-to-peer property exchange platform based on blockchain and its newly-appointed adviser Ian Taylor, former Minister for science, space and technology, and chair of several Parliamentary science committees, said: “TrustMe is a company with great potential and is a genuinely exciting proposition for anyone with an interest in the real-world applications of blockchain. The technology is steadily maturing into an effective means of improving a range of processes - in this case, TrustMe is deploying blockchain to change the way property is transacted which could enable property owners and developers very efficiently to unlock equity in their assets.”

Leisure adopts DLT

Knowing that Disney Resorts has run its loyalty and ticketing on blockchain for several years ought to be all the proof you need that this is a robust, scalable and credible technology. With the open-sourcing of its solution as Dragonchain, that platform has become a secure, serverless, scalable, cloud-based solution that any business can adopt (assuming it has purchased the necessary dragon tokens issued during its initial coin offering or ICO - see below).

Knowing that Disney Resorts has run its loyalty and ticketing on blockchain for several years ought to be all the proof you need that this is a robust, scalable and credible technology. With the open-sourcing of its solution as Dragonchain, that platform has become a secure, serverless, scalable, cloud-based solution that any business can adopt (assuming it has purchased the necessary dragon tokens issued during its initial coin offering or ICO - see below).

Another business named for the same mythical creature, gaming distribution platform Dragonfly which has over 100 million monthly active users worldwide for titles like Game of War, is adopting blockchain through the DCore solution developed by DECENT. It is aiming to reduce advertising inefficiencies, managing digital rights for the 60% of gamers who play offline, and reduce the cost of making SMS payments for gamers (where mobile operators currently take a 50-70% commission).

“Our co-operation with DECENT will bring all the advantages of blockchain technology to e-gaming. It’s gonna be a real gamechanger,” according to Dragonfly CEO, Kalvin Feng.

The same platform is also being deployed by Pivotal Entertainment, a media business which specialises in the film, television, music, publishing and fashion worlds. “Blockchain technology revolutionises the way entertainment is created, consumed and monetized,” according to Pivotal founder Amorette Jones. “I sought out DECENT because we share a common vision - to restore value to creative artists who are the lifeblood of entertainment.”

Charities are banking on blockchain. (So are banks.)

Giftcoin is set to launch its ICO on 11th December with the intention of using blockchain to make donation tracking more transparent. By converting fundraising cash into its cryptocurrency, that value can be tracked end-to-end by donors and causes giving a closed feedback loop and immutable proof of transactions. (Interestingly, this is parallel to the personal information use case I proposed in response to charities’ annus horribile.)

Lady Astor of Hever, a 20-year veteran of fundraising for charities including Parkinson’s UK and her main focus, The National Autistic Society, has welcomed the new solution. “Giftcoin is a revolutionary concept for charitable giving that shows the route from pound to project. This is exactly the kind of transparency revolution the charitable sector needs in the 21st century. It is an open, protected and satisfying digital method of giving,” Lady Astor said.

Alex Howard, co-founder of Giftcoin, added: “As the founder of a charity myself, I am all too familiar with the difficulty that charities face in connecting with the public and building trust. I firmly believe that transparency is key to solving this problem, and blockchain is the tool that will deliver it.”

With some predicting that blockchain and cryptocurrency will replace traditional banking methods within 20 years, it is no surprised that there is a scramble to be first-to-market with a credible financial services-oriented platform. Divi Project is led by a team including Tim Sanders, former Yahoo! chief solutions officer, Geoff McCabe, founder of Virtual Reality Times, and Toni Lane Casserly, co-Founder of CoinTelegraph, among other notable figures in the technology industry.

It is hoping to be a user-friendly cryptocurrency that could drive mass adoption, consumerising a technology that can seem opaque and even hostile to non-specialists. Given the failure of bitcoin’s fork - a technical measure to split the currency between its code-centred origins and new adopters - there is clearly space for this simplified approach.

But don’t get carried away - and don’t call tokens a security

Since the invention of bitcoin in 2009, there have been around 60 high-profile hacking incidents with the most recent seeing $70 million-worth of coins stolen. Most of these have been breaks in the cybersecurity protecting trading systems, rather than of the underlying encryption itself, but it is enough for Simon Bain, CEO of BOHH Labs, a San Francisco-based security start-up, to warn against seeing blockchain as hack-proof.

“While blockchain is a great tool for helping the security of transactions and making sure these are secure, this technology won’t secure the end databases. This is because, in practice, blockchain focuses on securing the external world and exchanges, but it does not look at the underlying security of the data. This is where blockchain adoptees need to be diligent,” he said.

Meanwhile, the US Securities and Echange Commission (SEC) has been keeping a close eye on all of those ICOs, subjecting many to a test to determine if they really are venture-funding exercises or attempts to create an unregulated security. In the UK, the FCA has issued a guidance note, although no new regulation has been forthcoming., while the European Securities Market Authority put out two sets of warnings, one for firms planning an ICO and the other for investors. At their simplest, ICOs just convert investors’ funds into a cryptotoken that can be spent using the service or used to fund the development of that service. But some have strayed across the line into becoming a security.

No doubt these issues will get resolved as blockchain continues to mainstream. For now, if you are taking a project to the board, you’d better be aware of any negative headlines and have a solution to offer in case your CEO calls you out on it.

Did you find this content useful?

Thank you for your input

Thank you for your feedback

You may also be interested in

DataIQ is a trading name of IQ Data Group Limited

10 York Road, London, SE1 7ND

Phone: +44 020 3821 5665

Registered in England: 9900834

Copyright © IQ Data Group Limited 2024